What is Your Portfolio Actually Made of? Part 2: The Capex Boom

In Part 1 of this series, I showed that 92% of the S&P 500's value now sits in intangible assets. Software. Algorithms. Intellectual property. A half-century of asset-light dominance that rewarded businesses with predominantly digital footprints, no factories to maintain, and no equipment to replace.

Three things are happening at the same time that put that model under pressure. The companies that defined asset-light growth are spending like industrial conglomerates, on chips, data centers, and power. The most profitable products in the global economy are no longer software subscriptions but physical components. And a competitive dynamic between the largest technology companies is ensuring that neither the spending nor the shift can slow down.

Read | Watch | Listen: Apple | Spotify

The Capital Investment Cycle

Capital investment cycles are generally tied to major technological shifts or structural demographic waves. Prior cycles include the Railroad boom mid 1800s, Telecom and Internet build out of the 1990s and early 2000s, the commodity supercycle of the 2000s led by China’s middle class construction boom, and the housing supply boom leading to the 2008 Great Recession. While each one of these cycles differs in size, scope, and importance, they all generally have similar features. Excitement around new technology or trend drives capital to be invested because of the prospect of high returns, more capital chases these returns, creating the boom and the ultimate oversupply. Capital gets destroyed, businesses fail, and industries consolidate until supply and demand can be in balance.

In my opinion, we are deep in Ai investment cycle right now, with the ultimate benefit of this technology to flow to consumers. There will be some pain along the way.

The Capex Shift

“Morgan Stanley estimates that tech companies will spend $2.9 trillion on chips, servers, and other pieces of data-center infrastructure between 2025 and 2028.”(1) The asset light erra is long gone. All that matters now for investors is what the return will be on this investment. That is THE Question.

Q1 2026 earnings season pointed to more investment. Some highlights. (2)

Microsoft – “For calendar year 2026, we expect to invest roughly $190 billion in capital expenditures [vs. $153.7bn consensus], which includes approximately $25 billion from the impact of higher component pricing. We remain confident in the return on these investments given higher demand signals and increasing product usage as well as the efficiencies we're already driving across the platform.”

Meta – “We anticipate 2026 capital expenditures, including principal payments on finance leases, to be in the range of $125 billion to $145 billion, increased from our prior range of $115 billion to $135 billion. This reflects our expectations for higher component pricing this year and, to a lesser extent, additional data center costs to support future year capacity.”

Amazon – “As we've been sharing, the faster AWS grows, the more short-term CapEx we’ll spend… The free cash flow in ROIC for these investments are cumulatively quite attractive a couple of years after being in service. However, in times of very high growth, like now, where the CapEx growth meaningfully outpaces the revenue growth, the early years, free cash flow is challenged until these initial tranches of capacity are being monetized and revenue growth outpaces CapEx growth.”

Importantly, there are two notable trends. (2)

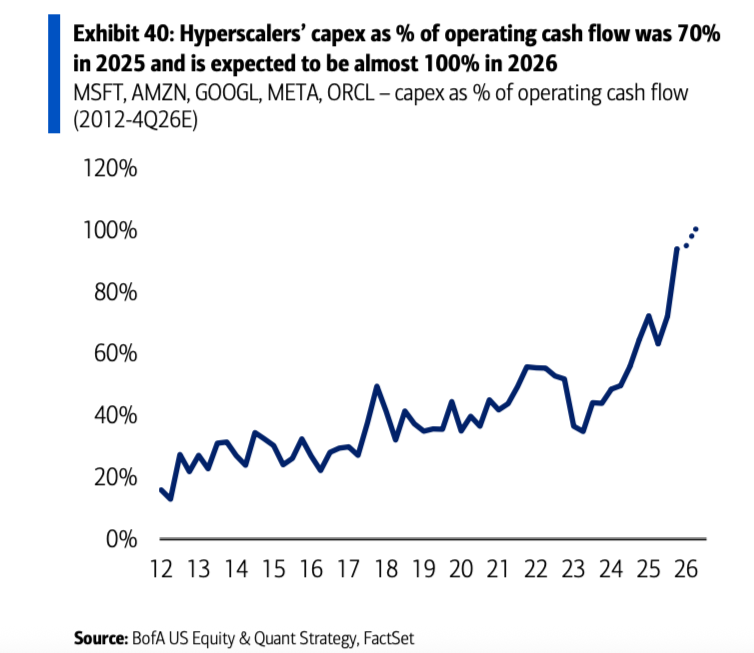

Hyperscalers’ (MSFT, GOOGL, META, ORCL) capital investments are now approaching 100% of Free cashflow in 2026. How much debt will be needed to continue this cycle?

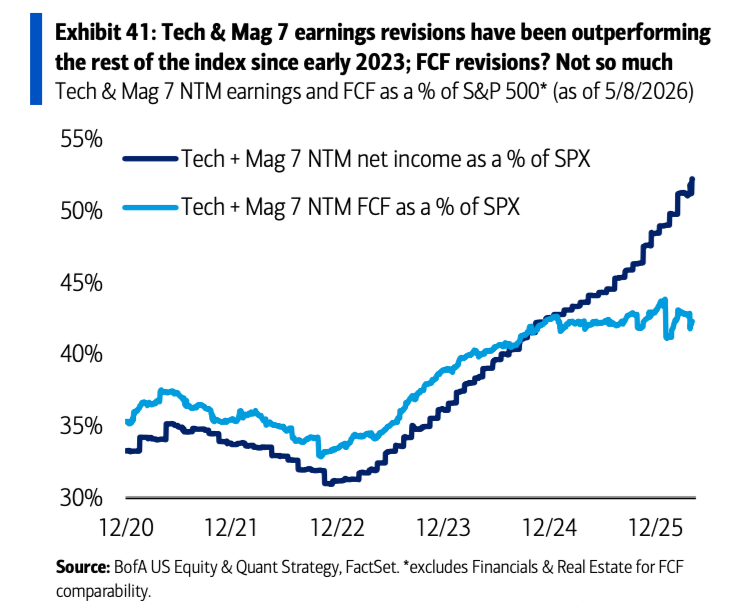

Earnings estimates for the MAG 7 continue to explode higher, Free cash flow growth, not so much. The difference being investments are not expensed they are depreciated, limiting the immediate impact to earnings. When do these large investments start impacting the income statement in a more meaningful way? Will the capital investment deliver the revenue and margin lift the street is seeking?

What has the Capex boom created? The Semiconductor Inversion

For a generation, physical manufacturing was the low-margin side of the technology business. Software was the high-margin side. That relationship is inverting.

Samsung reported first-quarter 2026 net profit equivalent to more than $30 billion, nearly matching the company's previous full-year record in a single quarter. Ninety-four percent of operating profit came from semiconductors. Samsung is now projected to be the second most profitable public company in the world this year, passing Alphabet, Microsoft, and Apple. A year ago, it ranked 16th (3)

Samsung, SK Hynix, and Micron, the primary DRAM suppliers, are collectively expected to generate roughly $350 billion in net profit for 2026. Each company is now projected to be in the top 10 most profitable companies in the world in 2026: 2nd, 6th, and 9th, respectively. Last year they were 16th, 18th, and 49th. Mind boggling. (3)

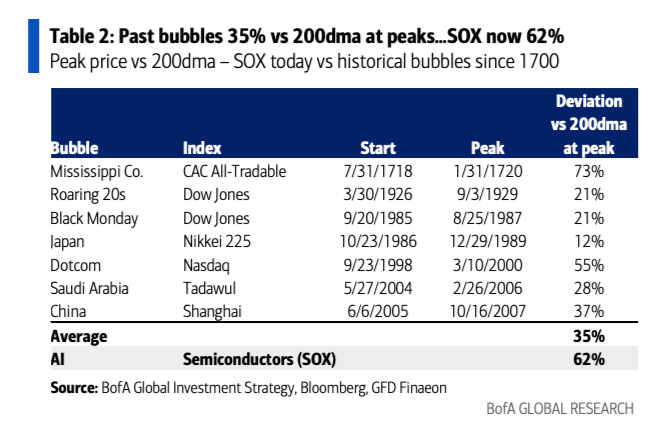

This shift in profitability has driven an explosive move in most semiconductor stocks beyond just memory providers, to a level that whispers “bubble.” Impossible to say, but the price action is in rare company. (4)

Why is this happening? Enter the Prisoner’s Dilemma

Every earnings call of note delivered the same message in different words: The spending will continue.

Classic prisoner’s dilemma. Hyperscalers are all competing for the same position in AI infrastructure. They cannot individually pull back and risk losing ground to the other, or worse, risk technological obsolescence. The cost of falling behind is existential. So it’s in their best interest to spend. And in doing so, collectively, they risk oversupplying the market, limiting returns.

Market leaders are becoming more capital intensive, more cyclical, and more dependent on physical bottlenecks than the last decade’s valuation framework assumed. That raises the importance of cash flow, balance sheet strength, and where in the chain the real returns are actually accruing.

The Wall Street Journal, "Big Tech Strikes Gold With AI, but at a Steep Cost," April 29, 2026

BofA Securities, Earnings Tracker Week 4, May 11, 2026

The Wall Street Journal, "AI Has Made Memory Chips One of the World's Most Profitable Products," April 30, 2026

BofA Securities, The Flow Show, May 14, 2026