SpaceX IPO: What Investors Need to Know

The blogosphere, financial and political pundits, are all upset over the recent record setting SpaceX IPO. Generally upset about the size, valuation, float, anything and everything to do with it. They are blinded by political biases due to affiliation of Elon Musk and the current administration. I will not opine on whether SPACEX is a good investment, but instead focus on how to actually think about the IPO, debunk a few of the biggest complaints, and close the loop on this series, if you haven’t read the first two they provide some detail to how we arrived at this pending IPO boom.

Part 1: In Part 1, I showed how the S&P 500 flipped from roughly 83% tangible assets in 1975 to 92% intangible today, an asset-light era built on software, brands, and IP that rewarded investors for a generation.

Part 2: In Part 2, I showed how that same asset-light model is now inverting, with the Mag 7 spending like industrial conglomerates on chips, data centers, and power, and memory makers like Samsung suddenly out-earning the software giants that used to define the market.

Read | Watch | Listen: Apple | Spotify

The SpaceX IPO and the vitriolic media response.

From an IPO perspective, the SpaceX offering was largely a success. A modest move higher (by IPO standards), retail participation, and orderly trading. But despite a successful IPO day, there are a litany of complaints. I’ll try and break them down one at a time.

The IPO valuation is too high at $1.77 trillion, approaching 100x sales.

This is correct by any conventional measure…But…

Elon’s compensation package centers around SpaceX reaching specific Market cap milestones up to 7.5 trillion AND the establishment of a permanent human colony on Mars with at least one million inhabitants. Wild.

Venture capital firm A16Z wrote regarding this compensation: “The board members who signed this package spent two decades watching Musk make predictions about SpaceX that sounded impossible before they came true. He said SpaceX would put humans in orbit when no private company ever had; it now flies NASA’s astronauts routinely. He said it would land and reuse an orbital rocket when the entire industry treated boosters as disposable; SpaceX has since done it hundreds of times. He said a satellite internet business could be worth tens of billions when satellite internet was a graveyard of bankruptcies; Starlink’s revenue has climbed from zero to $11.4 billion in a few years. The predictions were often aggressive on timing but almost never wrong on direction. And the original direction, written down in 2002 as the company’s mission, was to make humanity multiplanetary. So the board tied his pay to the mission itself.” (1)

Back to the valuation argument. Yes, by any traditional or even generous valuation argument, the company is overvalued. The best way to view the stock is as a “call Option” on a wild future. And this is where all the practitioner level perspective comes into play: Are you going to be around for this wild future? Are you spending down assets vs accumulating? Position sizing, rebalancing etc….

The float is too “thin”.

Translates to there is not enough shares available to be traded; As Musk critic Scott Galloway put it “Manufactured Scarcity”(2) to create a pop in shares.

SpaceX already ran the largest IPO in history, raising about $75bil in equity. Just release more shares is a straw man argument and misses the trade off the board has to make between raising capital, diluting shareholders, and managing control of the company. Just issue more shares is a lazy argument.

The SpaceX shares traded between 20 and 30% higher most of the IPO day. A near picture perfect, “average” IPO performance.

There are numerous lock up lifts over the next 180 days, allowing insiders to sell, providing plenty of liquidity.

Forced index buying will hurt investors.

The argument being, forced index buying will provide exit liquidity for insiders, leaving retirees to bear the brunt of a fantasy stock.

Investors have largely benefited from market indexation and the committees that run them. It is their stated objective to invest:

Stated objective of the Russell 1000: “Provides an unbiased, complete view of the US equity market and underlying market segments”

Nasdaq 100: “A globally recognized index of the 100 of the most innovative large cap companies listed on the Nasdaq Stock Market.”

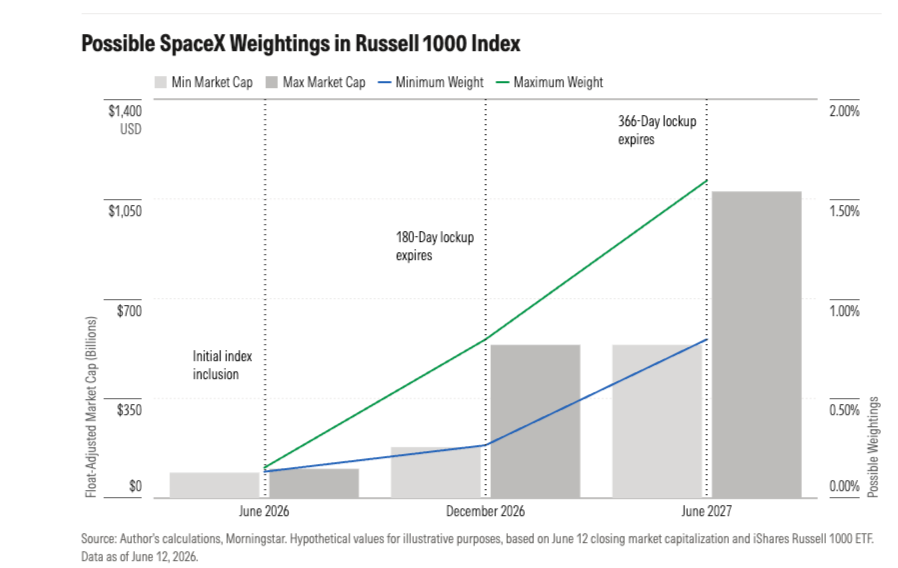

The Indexes will massage this in. For example, Per MorningStar (3).

Vanguard Total Stock Market ETF VTI will initiate at less than 0.20%

After 1 year, Estimates of about 1% in broad, cap weighted indexes like the Russell 1000, possibly north of 2% for Nasdaq.

The S&P 500 will not be purchasing inside 12 months and holds its profitability requirement.

The Dash for Cash

Here is what gets lost in the SpaceX inclusion debate. While the index quietly makes room for a nearly $2 trillion entrant, the giants already inside it are issuing debt and equity at a pace we have not seen before.

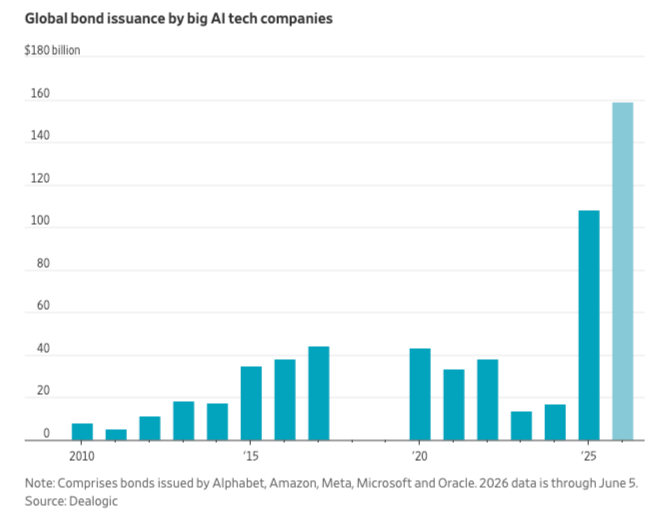

As I noted last month, tech companies are estimated to spend $2.9 trillion on Ai infrastructure between 2025 and 2028. This investment by Big Tech now exceeds their capacity to fund it via their cash flow generated from their businesses. Alphabet, Amazon, Meta, Microsoft, and Oracle have issued $159 billion in new debt this year (4); on top of this, Alphabet raised another $45 billion in equity capital with another $40 billion via an at-the-market program to begin in the third quarter. Nvidia even got in on the action, raising $25 billion in debt for “general corporate purposes.” There are a ton of possible reasons for Nvidia’s debt issuance, but I find it odd given their apparent “ability” to generate hoards of cash.

Why does this matter to investors? These investments, in sizes never seen before, must generate a return in excess of each business’s cost of capital. The idea that excess returns can accrue to everyone, model providers, hyperscalers, infrastructure providers, and end users is fallacy.

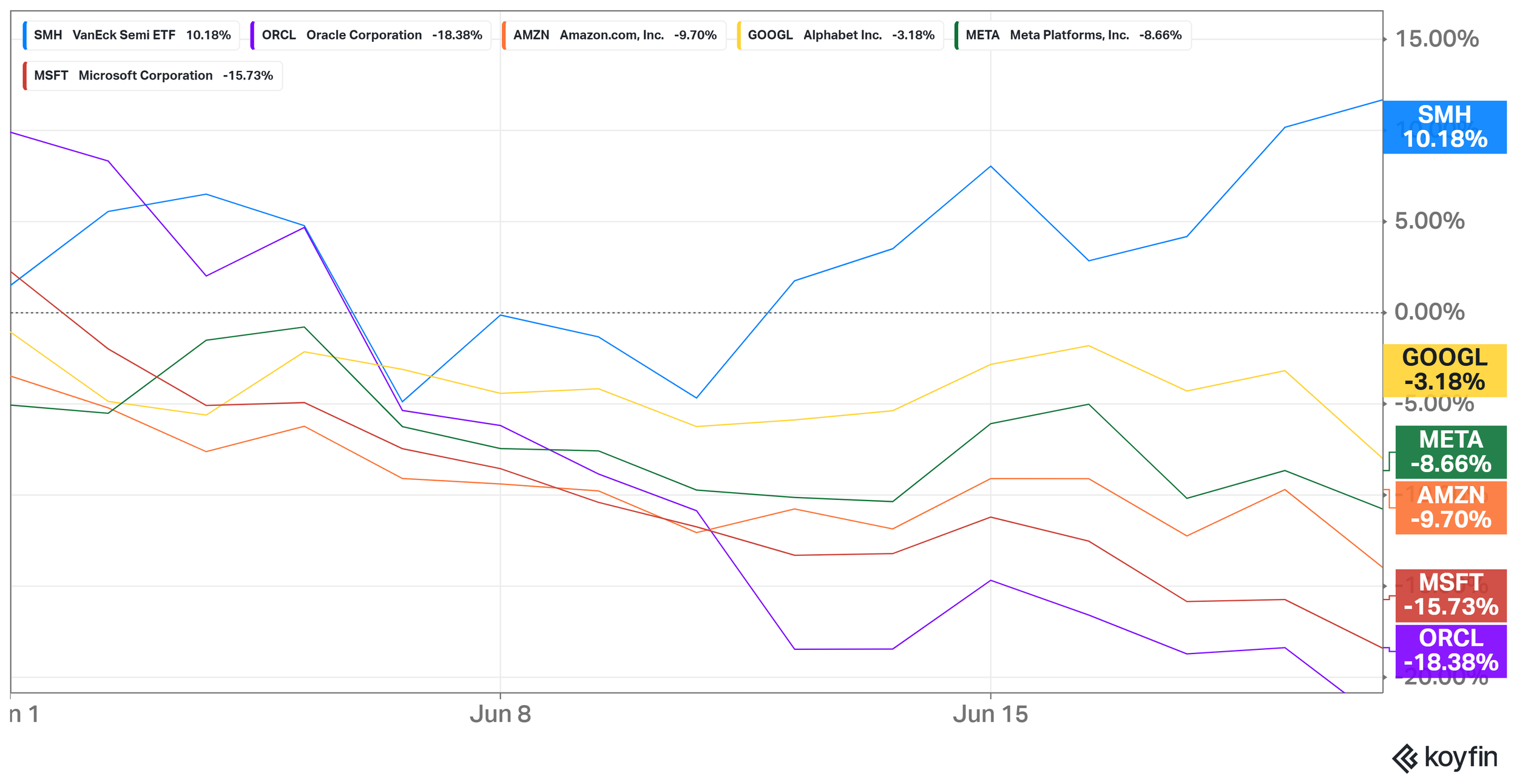

What is notable, is the performance spread between Semiconductors and the hyperscalers has become really pronounced in June. It would be different if they were moving down together, but the spread is what’s important.

MTD thru June 18 26

Some Possible reasons:

The incremental AI investment by the hyperscalers is seen as a negative, and the value will accrue to the semiconductor companies.

The market fears additional equity raises will come from hyperscalers after Alphabet’s nonchalant capital raise. Note: Google last raised capital at its IPO in 2004.

This spread is unrelated, and the recent SPACEX IPO was funded to some degree by selling the largest stocks in indexes.

All these are likely playing a factor to some degree, picking the biggest culprit is a guess. But one thing I feel strongly about is that the longer this spread persists and the bigger it grows, the more likely hyperscalers will push back. If the market does not reward the investment, they will moderate it.

We only have to look to Meta’s metaverse push in 2021 / 2022; the market did not approve and crushed the stock (-70+%), forcing Zuck to pivot.

What are the critical points for the remainder of 2026?

Will a hyperscaler blink on their capex investment?

Will Both OpenAI and Anthropic IPO in 2026, and who will be first?

Can the falling energy prices be enough to keep the Federal Reserve from raising rates?