What Is Your Investment Portfolio Actually Made Of? Part 1

You’ve spent 30 years investing and building wealth. But do you actually know what got you here? What is your portfolio actually made of?

Not the names on the statement. Not the fund tickers or portfolio managers. What is the underlying value of your wealth built on?

Most do not. Nobody has ever stopped to explain that the stock market has quietly transformed over the last half-century into something fundamentally different from what it used to be.

Here’s what changed.

The Portfolio You Can’t Touch

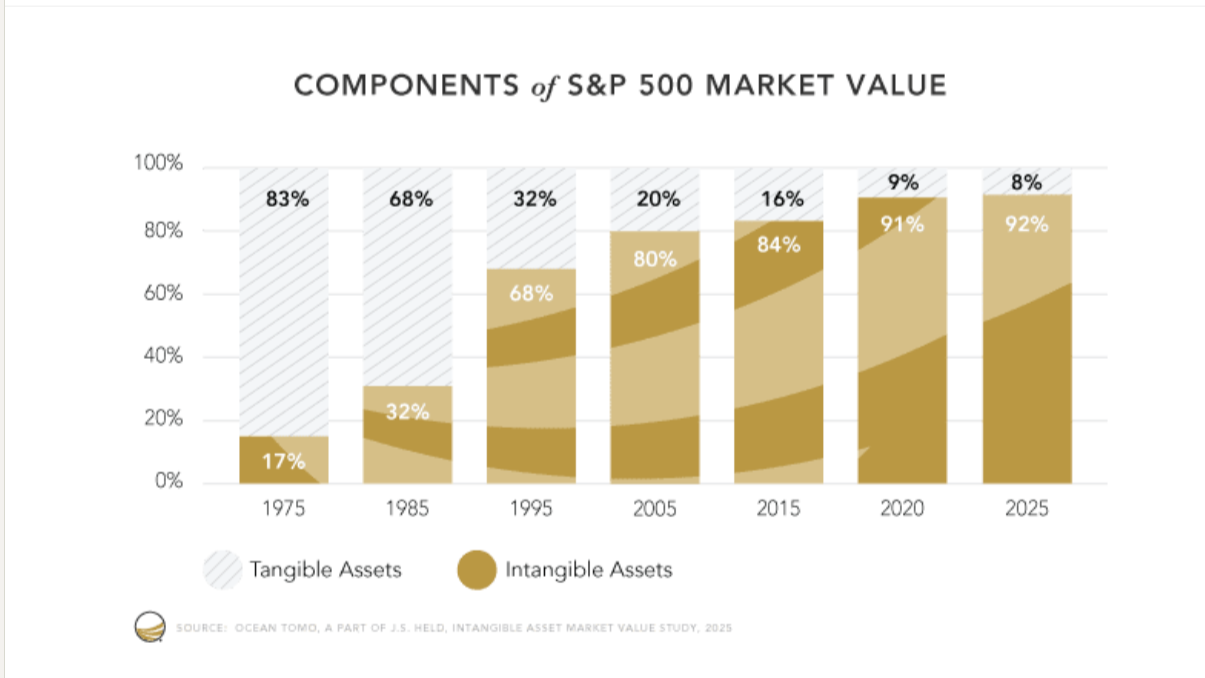

In 1975, the S&P 500 looked radically different. Roughly 83% of its value was tied to physical assets. Factories. Machinery. Land. Buildings. Equipment. Things you could see and touch.

Today that number is 8%

According to the 2025 Intangible Asset Value Study released by Ocean Tomo, 92% of S&P 500 market value is now intangible. Software. Brands. Algorithms. Intellectual property. Copyrights. By definition no physical substance.

Why It Happened

This wasn’t an accident. It was the natural result of an economy that moved away from manufacturing and toward services. Services now account for roughly 70% of U.S. GDP. We stopped making things, and started selling ideas, software, and expertise instead. It’s more profitable.

The purest expression of this shift is software. A software business, at its best, is a capitalist dream. You build the product, then you sell it a million times. Even better you build the product and charge every person that uses it a subscription. Each additional sale runs at essentially no marginal cost. No additional raw materials. No additional factory space. Just cash, pure leverage.

Mark Andressen saw this coming in 2011 with his seminal piece, “Why Software Is Eating the World.” (2)

“More and more major businesses and industries are being run on software and delivered as online services—from movies to agriculture to national defense. Many of the winners are Silicon Valley-style entrepreneurial technology companies that are invading and overturning established industry structures. Over the next 10 years, I expect many more industries to be disrupted by software, with new world-beating Silicon Valley companies doing the disruption in more cases than not.”

And he was right, in just about every way.

Look at the businesses that define the modern market.

Google Search is arguably the greatest asset-light business ever built. Each additional search costs essentially nothing to run. The asset is the algorithm. Microsoft built a software licensing and subscription empire sold to a massive installed base, with development costs spread across hundreds of millions of users. Salesforce pioneered the subscription model, adding seats and recurring revenue with almost no marginal servicing cost.

Even Nvidia, the market darling at the center of the AI boom, runs what's called a fabless model. It designs the chips but owns none of the factories that manufacture them. TSMC and others handle production. Nvidia's value lives entirely in its intellectual property, its software ecosystem, its engineering and design. No multibillion dollar plants to build, insure, or maintain.

Even companies outside of tech are in on the asset-light transition. Homebuilders prefer to contract lots via option rather than holding land on their balance sheet. Retailers have sold their real estate and lease it back to remove it off their balance sheet. Major hotel groups franchise our manage under contract hotels, rather than owning the real estate.

Physical assets are expensive. They wear out. They require maintenance, replacement, and upkeep. Ignore them and risk technological obsolescence or risk becoming a liability. PG&E, the California utility, failed to modernize its aging grid and was held liable for billions of dollars in damages tied to wildfires caused by its deteriorating infrastructure.

Wall Street loves it. Fewer physical assets meant companies could grow without massive capital expenditures. More free cash flowed back into the business or back to shareholders. Asset-light has become religion and the defining characteristic of the 2010s.

Consumers got pulled into the same model. We lease our cars. We subscribe to our music, our movies, our books. Klaus Schwab, founder of The World Economic Forum, captured the trajectory bluntly: you'll own nothing, and be happy.

The Trade That Crushed It

To understand why this matters now, you have to appreciate just how well this trade has worked.

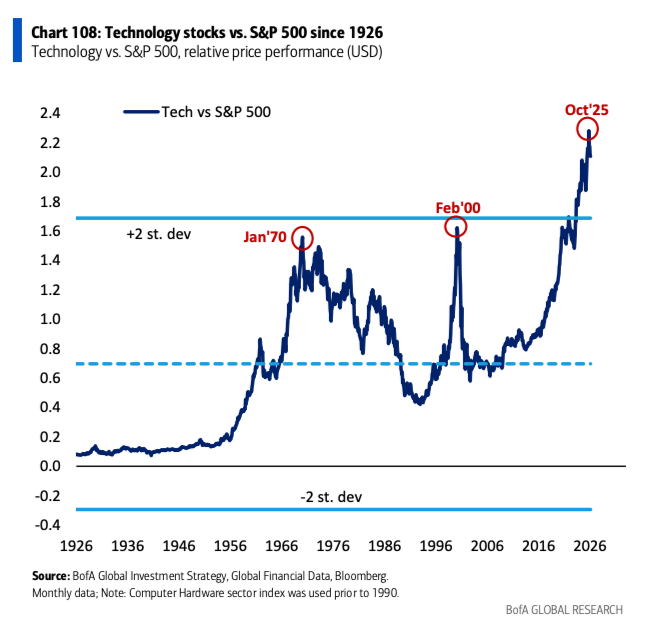

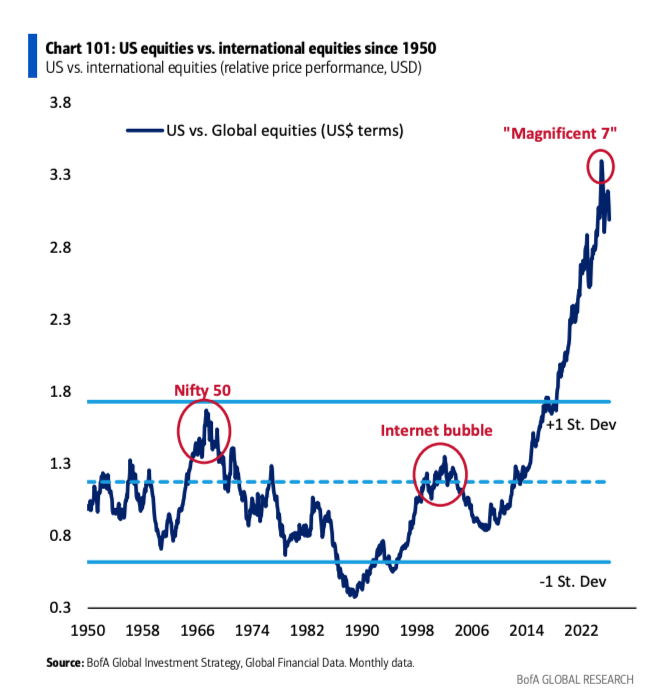

Technology stocks have ripped. No matter how you want to measure it, relative to other sectors of the S&P 500 and relative to the rest of the world.

The charts tell the story plainly. Technology stocks have outperformed the broader S&P 500 for a generation. U.S. equities have lapped the rest of the world. The Magnificent Seven didn't just participate in the market. They became the market.

This wasn't irrational. The market was pricing exactly what it got. Superior earnings growth, expanding margins, and the compounding advantage of businesses that scaled without proportional cost. The trade made sense. It still makes sense in pockets.

The question is whether the conditions that made it work are still intact.

The Question Nobody Is Asking

Here's what I want you to sit with before the next post in this series.

The portfolio you own today is 92% built on things that have no physical form. That worked extraordinarily well during the era that created it. An era of falling interest rates, expanding globalization, and unchallenged software dominance.

That era is under pressure in ways that weren't true five years ago.

The world is changing. The fragility of asset-light economies was exposed by COVID. Supply chains that looked efficient turned out to be brittle. Critical materials flowed through chokepoints nobody thought twice about until they did. And now the very technology that validated the asset-light thesis, artificial intelligence, is forcing the companies that defined the asset-light era to spend hundreds of billions of dollars on the most physical infrastructure imaginable. Data centers. Power.

The regime is shifting.

Most portfolios haven't.