The Iran War and Your Portfolio: History, Energy Risk, and What to Watch

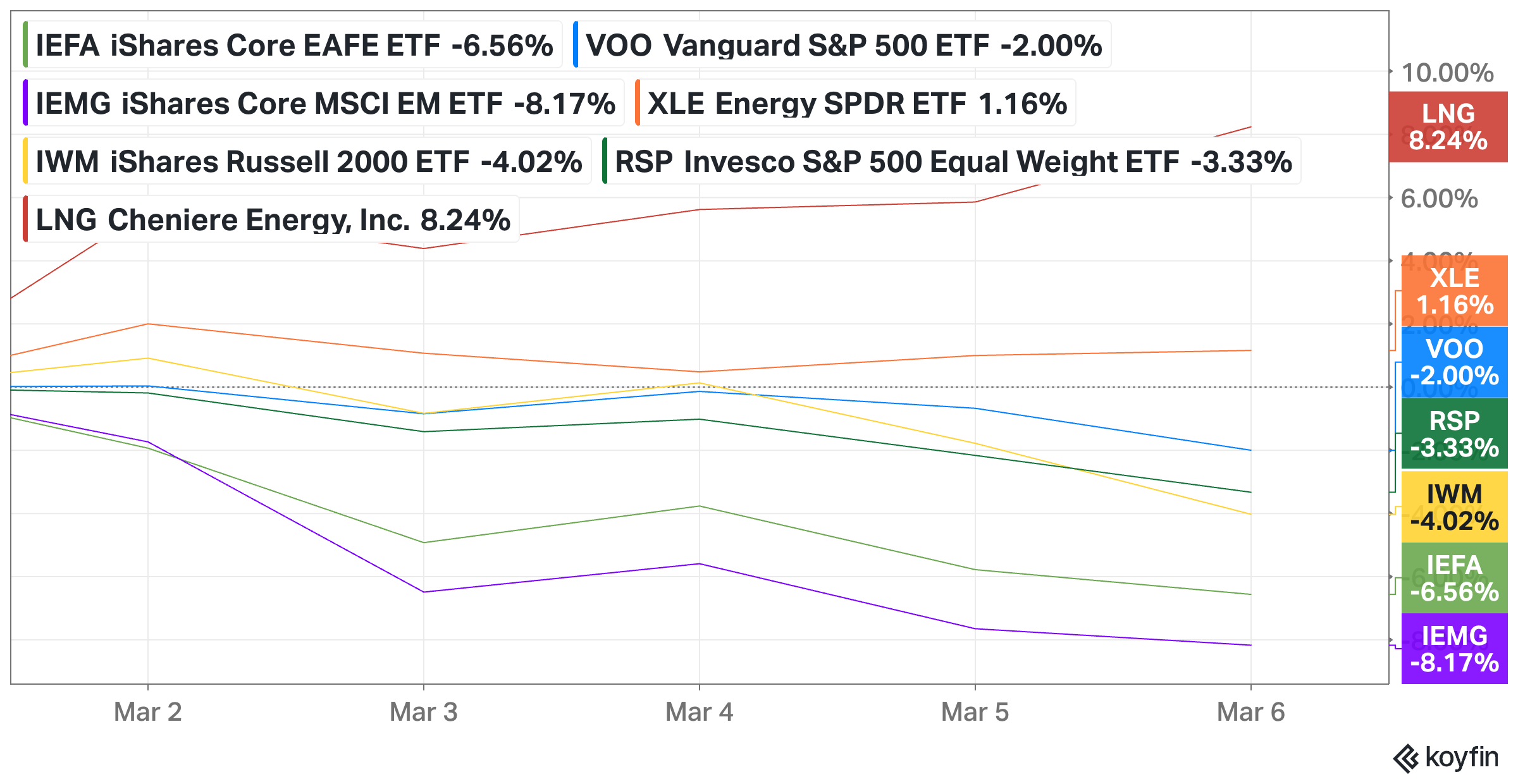

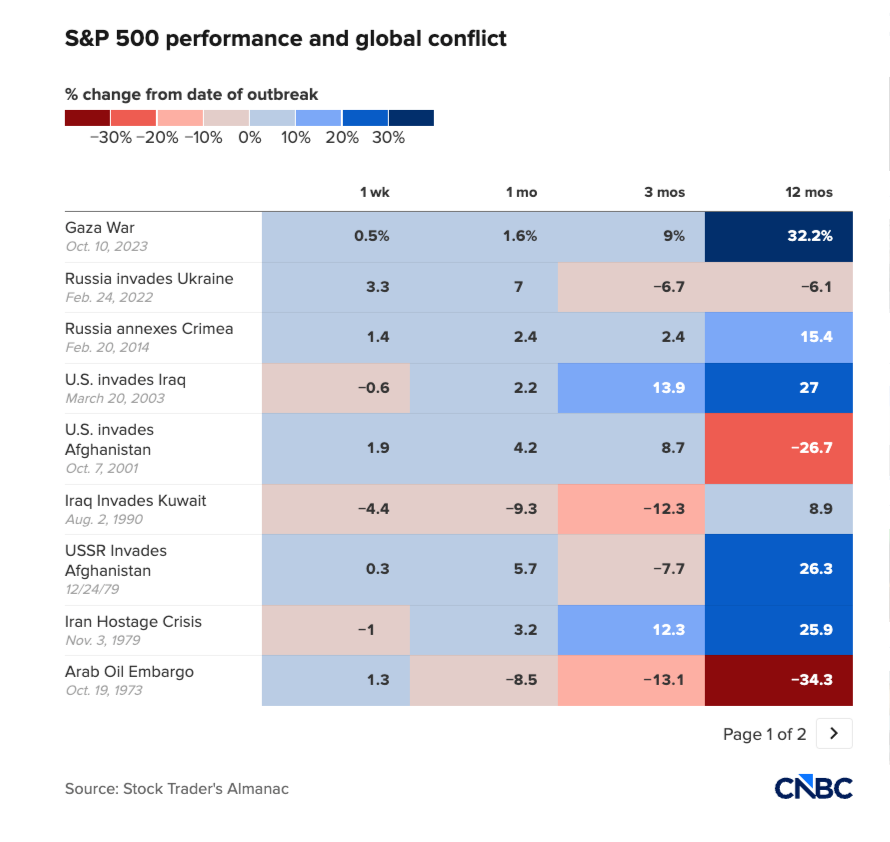

The S&P 500 fell just 2% in the first week of the Iran conflict, but the market rotation has paused: international equities, small caps, and cyclicals all underperformed. History shows stocks average stock market gains after geopolitical conflicts, but outcomes range from -34.3% to +32.2% With 20% of global oil transiting the Strait of Hormuz and crude futures pricing a short-term disruption ($73 Jan '27 vs. $91 spot), the market's bet on a quick resolution is the assumption to watch.

The US and Israel began joint air attacks on Iran on February 28th, and equity markets have been very resilient. Despite heavy selling pressure throughout the week, markets ended many sessions well off their lows. The S&P 500 ended -2% for the week.

However, a more detailed inspection of markets reveals a break in the rotation and broadening trend that began in 2026. International equities, US Small Caps, and the average US Stock all underperformed the first week of March as investors grapple with the duration, scope, and intensity of the war. The rotation isn’t dead, but it’s on pause.

The primary question for financial markets in the weeks to come: are we dealing with a short-term energy supply disruption or a durable supply shock?

What does history say about investing through war?

Most financial media point to the average gain after the conflict begins. The New York Times highlights the average stock market gain after U.S attacks lasting more than one day to be 12.5% one year after the start of the conflict, starting with Operation Desert Storm. (1)

CNBC highlights the average gain after the start of a global conflict 12 months later as 2.9% since World War II. (2)

All fine. But, it misses the range of outcomes and concurrent market dynamics. For example, the US invaded Afghanistan in October of 2001, with the market down 26.7% a year later. Do we attribute the negative performance to the war or to the continued unwind of the technology bubble that burst the prior year? It was likely multiple factors all colliding at the same time.

Why the “do nothing” playbook carries more risk.

There are four conditions that are converging on markets that make this conflict different in my view.

Valuations and Concentration. As I wrote in February, the S&P 500 sits at historically high valuations with unique technology concentration risk.

Energy is structurally under owned. Energy equities carry an insignificant weight in the S&P 500. As a percent of the S&P 500, the energy sector accounts for 3.5%. For the Nasdaq 100 its even less at 0.6%

The Fed could be in a bind. Rising energy prices make reducing interest rates incrementally harder for the Fed. This element remains key for reducing consumer cost and fueling the broadening of stock market performance.

It’s hard to remove China from the equation.

“China buys 80% of Iranian oil at steep discounts, it committed $400 bn of investment in Iran as part of a 25-year strategic partnership, it built most of Iran’s surveillance network, it recently planned to replenish Iran’s ballistic missile stockpile and sell Iran supersonic anti-ship cruise missiles. China’s objective: tie the US up in the Middle East and reduce its capacity for any response regarding Taiwan.”

What is an investor to do?

Assuming you haven’t adopted my mantra of “managing risk before it is present,” let’s explore three common decisions an investor might make.

Buy Energy Equities?

Remember, the market is a discounting mechanism, assessing the possible future outcomes and bringing prices forward. Energy equities measured by XLE are up 26% YTD through March 6th, with a bulk of the gains coming before the conflict. It should come as no surprise that military assets were moving into the region, and energy equities were climbing. This also explains why the energy equities haven’t really moved in response to oil prices; equity markets look forward, already accounted for. Buying energy stocks today requires the view of a durable supply shock. Per the CME group, Crude oil priced for delivery in Jan 27 is $73 vs $91 today. Oil market says this is a short-term disruption currently.

We also have to ask what a more stable Iran and Venezuela mean for long-term global supply dynamics. A positive war outcome may be a headwind for energy equities.

Reduce equity exposure?

The S&P 500 is about 3.5% off its all-time high. While I’m not a fan of reacting to volatility, if this conflict causes you financial worry, reviewing your underlying equity exposure now seems like a good idea. Get professional guidance as the where to reduce and how to reduce matters.

Buy?

For net savers, this is the time to get organized. Outline your cash demands over the next 12 to 18 months, make sure your financial house is in order, and prepare the surplus to be an investor.

Last week slowed down the market rotation occurring in smaller, cyclical, non-AI disruptable businesses. This is still an area of focus for my research efforts and where the greatest opportunities live.

What I’ll be watching.

What I’ll be watching to monitor the short term vs long term energy disruption timeline: XLE vs S&P 500 relative performance, 6 and 12 month brent contracts, the performance of Cheniere (LNG), the largest US LNG exporter, and big energy importer equity markets, Japan and Europe.

As of March 6th, 2026, the market remains resilient, and it’s still a bull market; act accordingly.