Back to Basics: What to do with Bonds in 2026 and beyond?

Markets moving too fast, AI agent commentary in video/audio

With the 10-year Treasury yielding just 4.05% against 2.4% inflation, bonds offer slim real returns, and the structural headwinds of geopolitics, deficit spending, and sticky inflation aren't going away. This post breaks down the bull and bear cases for bonds in 2026, explains when fixed income still makes sense (short-term expenses, retiree safety nets), and why long-term investors may want to review their Bond allocations. I’m not a fan of most bond indexes.

Certainty is nice, but it comes at a price. Today, Feb 14th, the 10 year US Treasury trades at a yield of 4.05%. The most recent CPI data marked inflation at 2.4%. Essentially, at current levels of inflation, a holder of this bond is loaning money to the US Government for 10 years at a real return 1.65% per year. And don’t forget, if you’re a taxable investor, you have to pay taxes at ordinary income tax rates.

Bonds have also been historically used as a volatility dampener; when stocks go down, so do interest rates. Investors flee to safety in periods of stress. This buying pressure drives rates down, and bond prices up, creating diversification benefits. But things have changed…

The global bond market entered a structural bear in January 2022 with a rapid rise in interest rates, in response to inflation accelerating after COVID related government spending. While the Fed has lowered short term rates, long term rates have remained relatively firm and hypersensitive to news around inflation, geopolitics, debt, and deficit spending. The weaponization of the US dollar reserves as a response to Russia’s invasion of Ukraine, and the use of tariffs to drive geopolitical outcomes, further complicates these dynamics.

The recent Greenland drama emphasizes this point. Tariff threats, plus the news of Danish pension fund announcing the sale of US Treasuries, caused the 10 year Treasury rate to rise to 4.3%. The pension fund selling $100 million in treasury bonds is completely irrelevant in size, but the signaling matters.

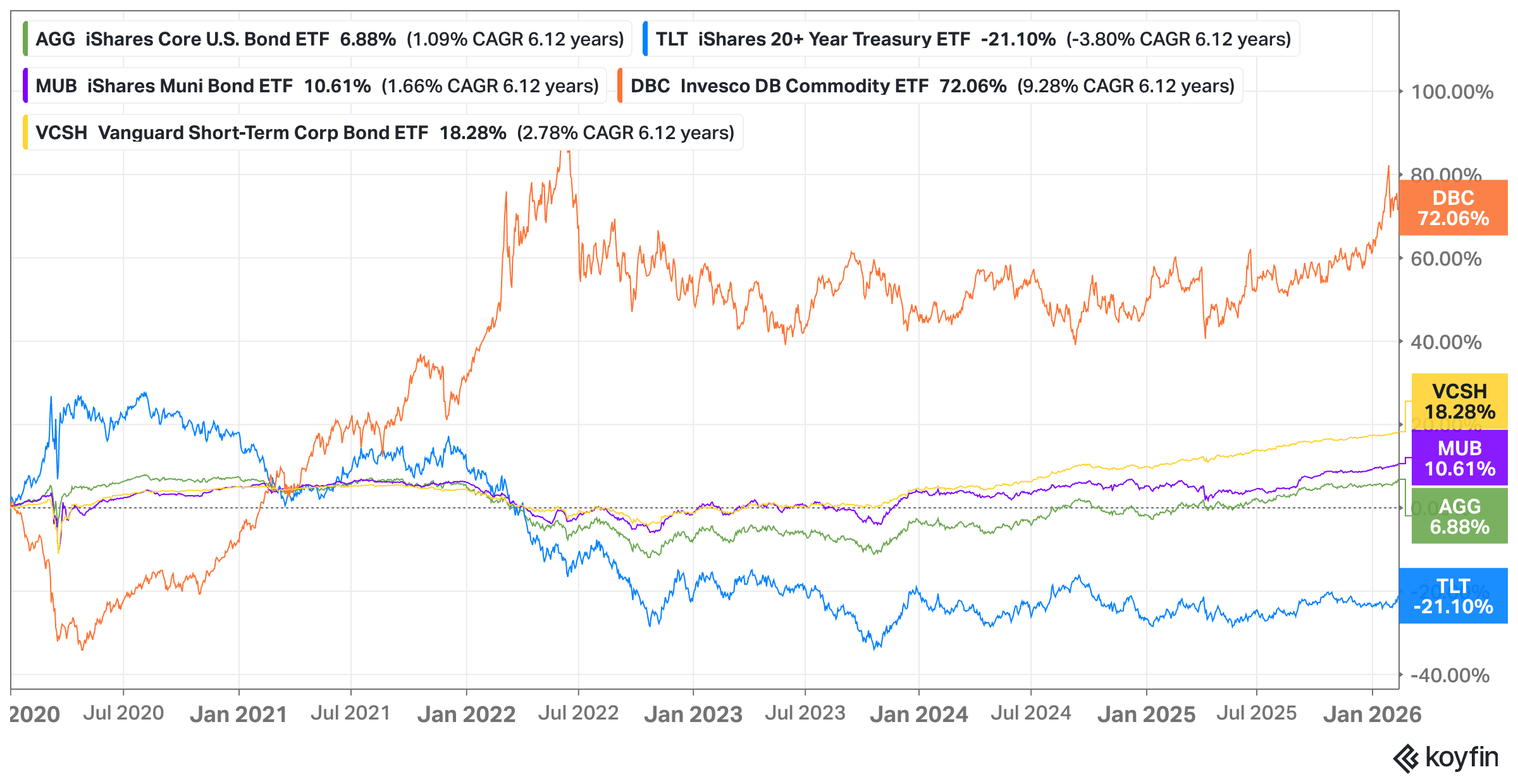

Returns for fixed income instruments have been poor, with most high-quality indices returning cumulatively less than inflation, and crushed by a commodity basket (including precious metals).

Jan 1 2020 - Feb 13 2026

So what do we do now? There are two paths in my view.

The equity bull case> AI leads to an inflection on productivity, the benefits of AI broaden, leading to an economic boom. Businesses can be disrupted by smaller incumbents. Competition shifts to a higher gear, and prosperity reigns. The higher nominal growth increases tax receipts and shrinks the deficits. The US government has a credible path to outgrow the debt burden. Interest rates are re-priced lower, reducing the interest burden and accelerating the improvement of the country's fiscal situation. I believe this is what Treasury Secretary Bessent is trying to orchestrate along with the newly nominated Fed Chair Kevin Warsh. A new accord to better sync the funding of US deficits and monetary policy operations, with the ultimate goal of decreasing the country’s interest cost. This scenario is a very bullish for equities.

The equity bear case> AI capex leads to bust. The K-shaped economy, the divergence between asset owners and workers, results in a fall of the upper “K”. High-income consumers and households rein in spending, and we get a recession. The country’s balance sheet and fiscal situation leave little room for error. Tax receipts fall, deficits widen, interest rates go up, and the traditional mechanism of rates going down fails. Rates go up in response to the country's debt burden. The Federal Reserve has to get creative, implementing some sort of yield curve control. Bad time for Bonds as real purchasing power is hurt due to higher inflation. The AI cohort of stocks has a real hard time.

While I present a binary scenario, real life is anything but. These possibilities sit on a spectrum, and we will likely land somewhere in the middle. However, the structural challenges for long term bond holders remain: firm inflation, global debt burdens, and capital warfare. And as I discussed in my prior S&P 500 piece, starting points matter, a 4.05% 10 year Treasury do not compensate for these risk.

YES. It must be strategic & purposeful, tied to a specific financial objective. Fear of equity markets is not enough of a reason today.

For all investors with expected expenses or cash outflows within 5 years, bonds can be used to provide certainty by matching maturity schedules to expenses. For retirees, bonds can serve as a safety net. Maintaining 3-5 years of living expenses in a “rainy-day” fund can fund your lifestyle in an equity bear market. Nothing is worse than selling equities down 20%+ to pay your bills. Draw down the rainy day fund, replenish when markets recover. The biggest risk for a long term time horizon, 10 years+ remains inflation, eroding purchasing power.

The reality is that the longer your time horizon, the riskier bonds are to your purchasing power. I reference my work bible, Jeremy Siegel’s “Stocks for the Long Run.” He highlights this dynamic:

“It is very significant that stocks, in contrast to bonds or bills, have never delivered to investors a negative real return over periods lasting 17 years or more. Although it might appear to be riskier to accumulate wealth in stocks rather than in bonds over long periods of time, for the preservation of purchasing power, precisely the opposite is true: the safest long-term investment has clearly been a diversified portfolio of equities.”

If this strategy brief raised questions about your portfolio or retirement plan, let’s talk. Schedule some time.