Back to Basics: How to Invest in 2026 - The S&P 500

The first installment of the 2026 Strategy Guide.

Valuation headwinds: Significant divergence between S&P 500 market cap and the Equally weighted S&P 500 forward return expectations.

AI investment uncertainty: The massive AI infrastructure spending by Mag 7 companies may not translate to sustainable margin expansion.

Software terminal value risk: Semiconductor stocks are surging while legacy software businesses are being sold off.

Forget price targets and forecasts. They are a fun exercise but provide no value. What matters is strategy, how to think about current dynamics to guide decision making.

What actually changes as we turn the calendar? For many investors, they return from the holiday lull and start making investment decisions again. After a strong year, everyone has considerable gains and why realize them in November or December and pay taxes in April. Instead they push investment changes to January, delaying the tax bill for 16 months. The calendar switch provides a natural opportunity to reassess, rebalance, and right size positions.

Before we dive into 2026, let’s check on my recent views. A few consistent themes have emerged since I began publishing.

Don’t get over yours skis on your AI exposure. (October Brief & December Brief)

The Mag 7 have a difficult set up. (September Brief)

Market rotation was beginning , MAG 7 to S&P 493 / Small cap.(September Brief)

Midterms drive political pressure to take action on consumer financing costs and housing. (November Brief)

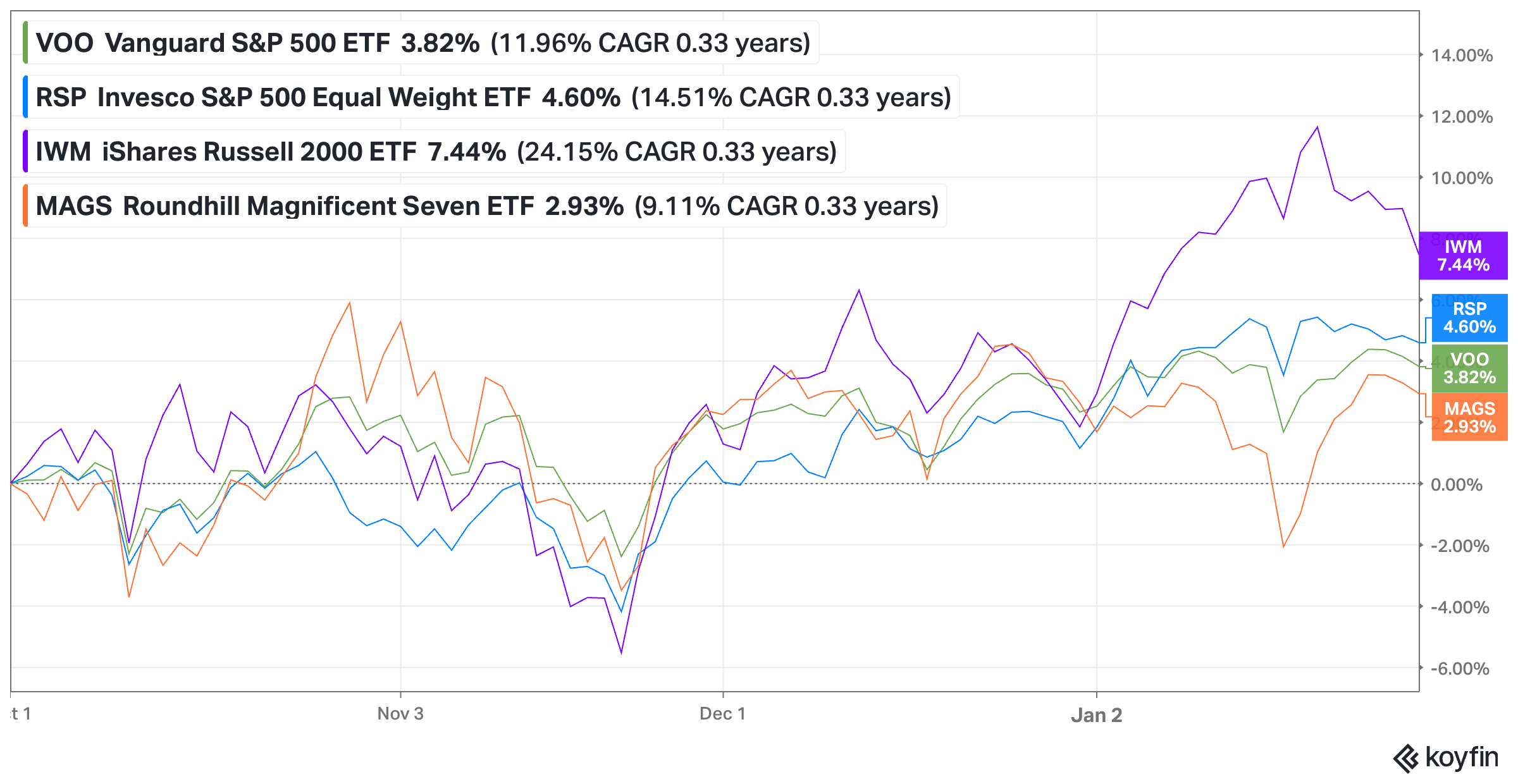

So what’s the score card? Since the beginning of the 4th Quarter 2025, small caps, the average stock (represented by the equal weight S&P 500), have outperformed both the traditional market cap weighted S&P 500 index and the Mag 7 (MAGS ETF).

My views in the 2026: Housing Shift have been mixed. On one had, the President instructed the purchase of Mortgage Backed Securities (MBS) by Fannie Mae and Freddie Mac in January, as I noted in the brief. On the other, the rate on the 10 year Treasury bond has been moved modestly higher.

10/1/25 - 1/31/2026

What’s my beef with the S&P 500?

Starting points matter, and the setup for both long term and near term return drivers are challenged.

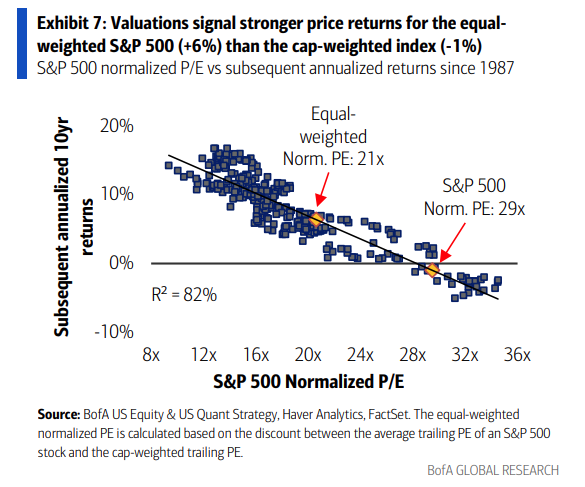

I still believe valuations are the primary driver of long term returns. Per BofA, 10 year annualized returns of the S&P 500 are set up to be negative, -1% per year.

The equally weighted index, invest $100 and each of the 500 companies receives 20cents, removes the outsized impact from the giant tech companies, is set up for more acceptable returns +6% per year.

Corporate profit margins have historically returned to average; they expand then contract. The main reason we sit at historical levels of valuation is profit margins of MAG 7 companies have continued to expand. These companies have been “asset light,” requiring less capital to generate increasing profits. This has begun to change with the AI investment cycle, as they spend record amounts of money to build AI infrastructure.

The challenge for investors, especially those approaching or nearing a phase that requires distributions from their portfolio, is we do not know how the return stream will unfold. Is it a 2000 style grind with three consecutive negative years, is it a crisis style blow up like 2008, or is it just a period of sideways returns?

As an active investor, these views lead me to a strategic direction. First, I don’t need to own all the Mag 7 cohort. Second, there is significantly more opportunity within the other size segments of the market that are tied to the real cyclical economy, rather than participating directly in the AI arms race.

Short term, the story has begun to shift. The market is questioning the AI spend, scrutinizing circular revenue deals, and asking when is the AI revenue coming. Since the beginning of the Q4 2025, performance of the Mag 7 has been unchanged, with the average S&P 500 stock outperforming.

The S&P 500 simply looks like a concentrated growth fund, and investors that have treated the index as a low risk buy and hold investment, could be running on borrowed time.

What is my view on the AI investment cycle?

While I’m not a Michael Burry disciple, his take recently featured on Dwarkesh Patel’s Substack, perfectly echoes my opinion.

“Warren Buffett owned a department store in the late 1960s. When the department store across the street put an escalator in, he had to, too. In the end, neither benefited from that expensive project. No durable margin improvement or cost improvement, and both were in the same exact spot. That is how most AI implementation will play out.”

The primary beneficiary will be consumers and small businesses with increased competition and lower prices. For the S&P 500 to produce decent returns, the AI investments will have to lead to a sustainable margin expansion for the Mag 7 group. The group is now battling amongst themselves, Amazon and Google developing their own TPUs competing with Nvidia’s GPUs for specific workloads, for example. The continuous need for infrastructure investments like data centers and electricity make margin growth difficult in my view.

On January 21st, Lemonade, the insurance company, announced a new offering specifically designed for self driving cars, starting with Tesla: “The new offering cuts per-mile rates for FSD-engaged riving by approximately 50%, reflecting what the data shows to be significant reduced risk during autonomous operation.”

This is just the beginning.

On the technological progress front. I return to Dwarkesh’s interview with Ilya Sutskever, the co-founder of OpenAI and former chief scientist. The title of the interview is “We’re moving from the age of scaling to the age of research.” My view on the interview was the push for Artificial General Intelligence will not be achieved from scaling LLMs. As the holy grail of AI tech gets pushed further out, the hypothetical value to investors today becomes less and less. Challenging the core of the AI narrative is being pushed to the forefront, rather than being fringe or contrarian.

What is a key trend that captures the AI investment debate?

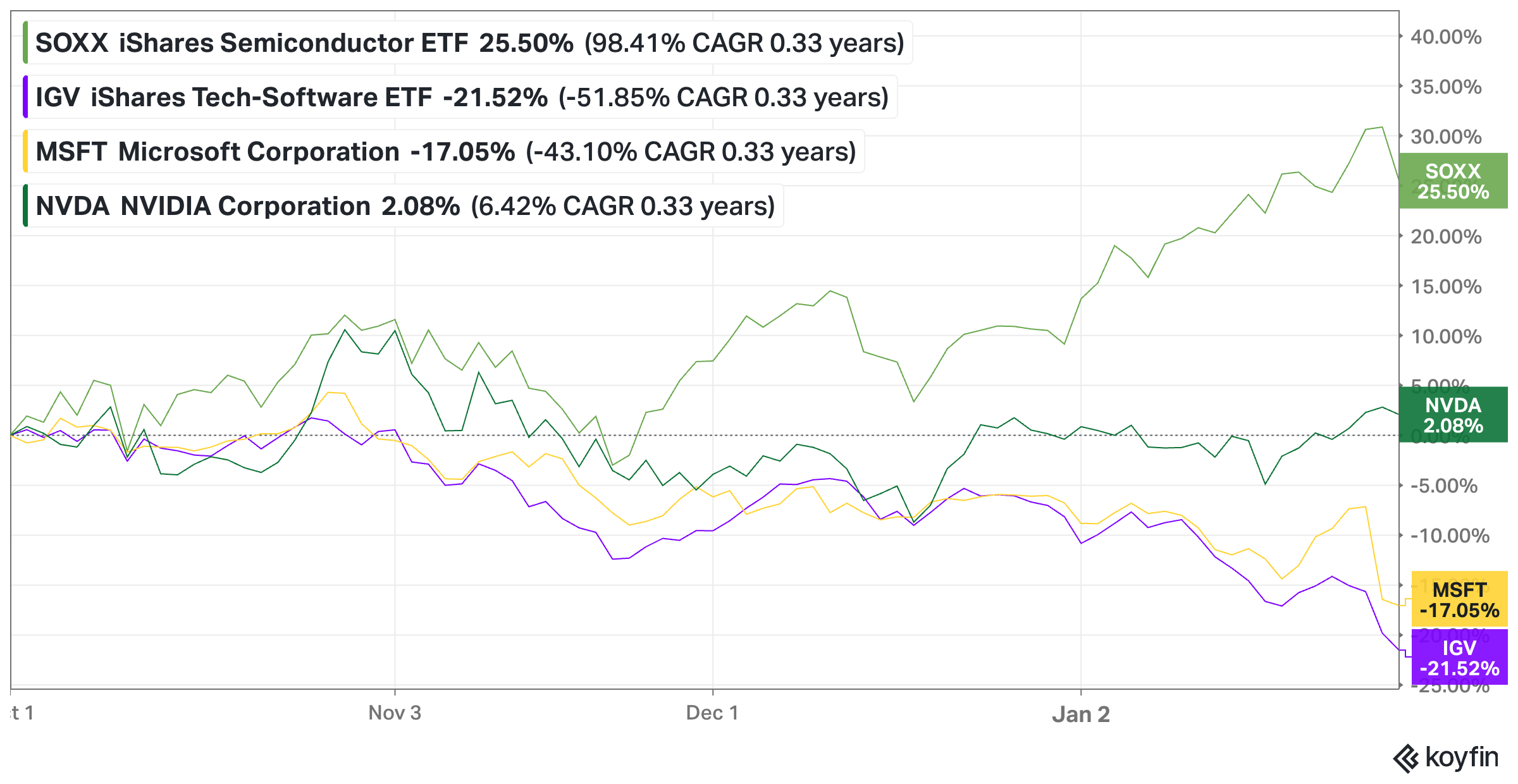

The price action between software stocks and semiconductors has diverged. This is the AI trade magnified. Investors are buying semiconductor stocks, the backbone of the AI infrastructure and selling legacy software businesses, reducing or eliminating their terminal value.

The best way to think about terminal value is the legacy automakers, GM and Ford. These businesses have traded so cheaply despite decent cashflows, because the market is saying “yeah you aren’t going to be needed or around in the future.”

Could this process be starting in the software stocks under the premise that companies can build their own software using AI?

If this strategy brief raised questions about your portfolio or retirement plan, let’s talk, schedule some time.