Maximize your quality of life : Social Security and Retirement Withdrawals

Maximizing Social Security isn't just about spreadsheets and life expectancy calculations. Prioritizing your health span and understanding spending behavior patterns can help you enjoy your wealth during the years that matter most.

You are not a spreadsheet, actuarial table, or financial model. Qualitative considerations, how we feel, enjoy, or may regret our financial position is equally as important.

When to claim Social Security benefits has largely been reduced to a lifetime benefit maximization equation based on your and your spouse's life expectancy. Pretty much, tell me when you are going to die and I’ll tell you when to claim your benefit.

“It’s silly to pretend that a dollar of retirement income at 62 is no different from a dollar of (potential) retirement income at 95.”

But my view has always been, Wealth Management is as much an art as it is math.

How we think about our wealth is unique to our individual experiences and qualitative considerations should be given to the timing of social security benefits.

Here are my two focal points:

Health Span - Prioritize enjoying money during healthier early retirement years.

Spending Behavior Patterns - Your are more likely to spend social security income than portfolio distributions. As odd as this seems, retirees don't spend their savings. I think at times there’s a conscious or subconscious fear of being poor (again).

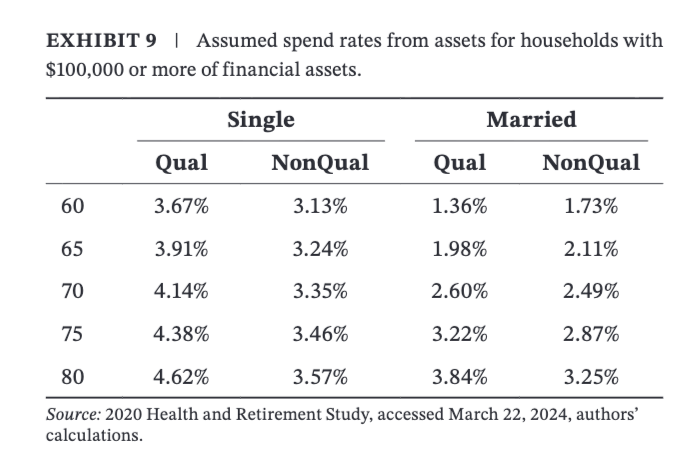

Recent Research in the Financial Planning Review, “Retirees Spend Lifetime Income, Not Savings”, highlights key points:

Retirees don't spend their savings, withdrawing about 2% at age 65. About half of the rule of thumb 4% spending rate, which many argue is also too conservative.

Most interestingly retiree spending rises as required minimum distributions (RMDs) from qualified retirement accounts begin.

Retirees are seeking permission to spend their own money. And without that permission they are hoarding wealth. Imagine subconsciously needing permission from the IRS.

Claiming social security prior to age 70 can help improve quality of life. Get specific advice.

Retire, Spend, and Give; Do it with a professional that will help you reduce anxiety and stress.

Your spouse will thank you. Your kids will especially thank you as they struggle with a home affordability crisis, and $1250 a month child care.

Sources for further review: